At present, the rapid development of electrification and intelligence in China's automobile industry is shaping and changing the preferences of Chinese automobile consumers.

In turn, the changing preferences of Chinese consumers have also had a profound impact on China's automotive industry. This mutual influence is not only crucial to the future of China's automotive industry, but will also profoundly affect the technological development, business model and competitive landscape of the global automotive industry in the next five to ten years.

2024 Beijing International Automotive Exhibition

Recently, McKinsey released a report on Chinese consumers’ car consumption behavior in 2024, which summarized five major trends:

First, the continuous introduction of new smart electric vehicles has increased their appeal to consumers, who are turning their attention more to mid- to high-end models. At the same time, price wars have limited impact on consumer decisions.

2. The premium halo of foreign and joint venture brands is disappearing, and traditional luxury car users are being attracted by Chinese luxury smart electric vehicles.

3. The penetration rate of electric vehicles is rising rapidly, and electric vehicle consumers are increasingly considering the performance of the car itself rather than incentives such as free license plates. However, as the deployment of electric vehicle charging infrastructure in some areas is slow, Chinese consumers' acceptance of electric vehicles has declined for the first time. It is urgent to accelerate the construction of charging infrastructure.

4. Chinese users prefer the "direct sales model", under which all links from sales to after-sales are more "transparent".

5. Consumers are very enthusiastic about autonomous driving technology, but are only willing to use it for free and are not willing to pay extra for autonomous driving technology packages.

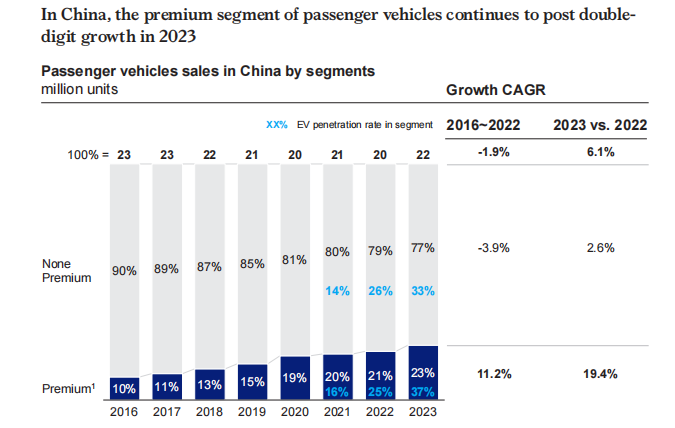

Smart electric vehicles lead the upgrade of automobile consumption

Looking at each item, the report shows that from 2016 to 2023, the proportion of mid-to-high-end cars increased from 10% to 23%. Among them, the growth of the mid-to-high-end market segment is also accompanied by an increase in the proportion of smart electric vehicles in China's high-end market. 37% of the 23% in 2023 are electric vehicles.

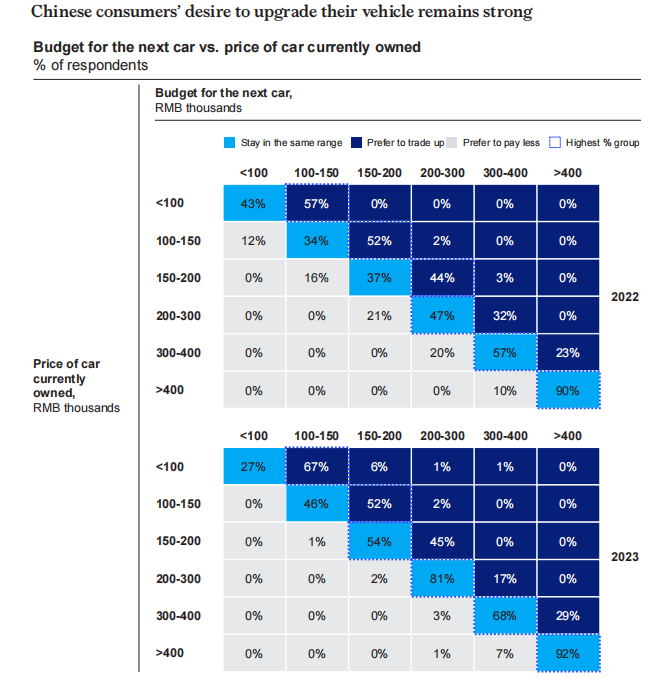

As can be seen from the figure below, regardless of whether existing users are in the 150,000-200,000 yuan, 200,000 yuan-300,000 yuan, or 300,000 yuan-400,000 yuan range, their desire to "downgrade consumption" when purchasing their next car has been greatly reduced. Most people said that their next car will remain in the current price range or even enter a higher price range.

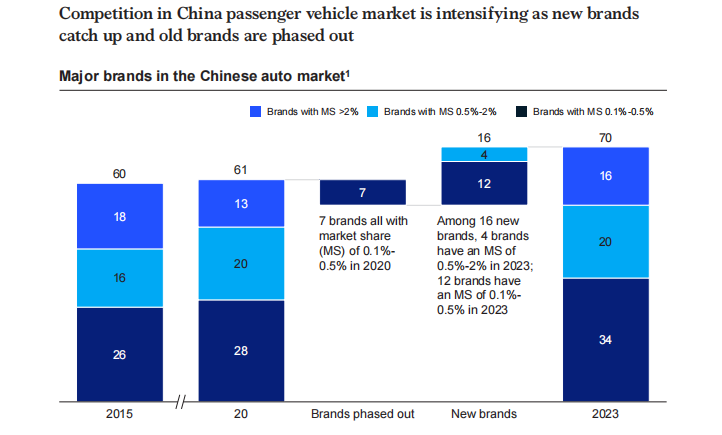

The halo of foreign brands has disappeared, and traditional luxury car users are attracted by Chinese brands

The report shows that from 2015 to 2023, 7 brands will fade out of the Chinese market, but 16 new brands will be born (only brands with a market share of more than 0.1% are counted). Among them, 4 of the 16 new brands have a market share of between 0.5% and 2%. This shows that emerging auto brands have diverted a lot of traditional brands' appeal.

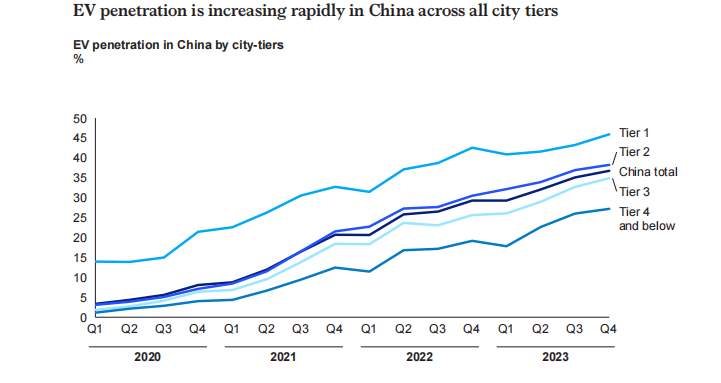

Consumers’ decisions have shifted from being influenced by policies to being attracted by the product itself

From 2020 to 2023, China's electric vehicle penetration rate will increase significantly. This trend is seen from first-tier cities to fourth-tier cities and below.

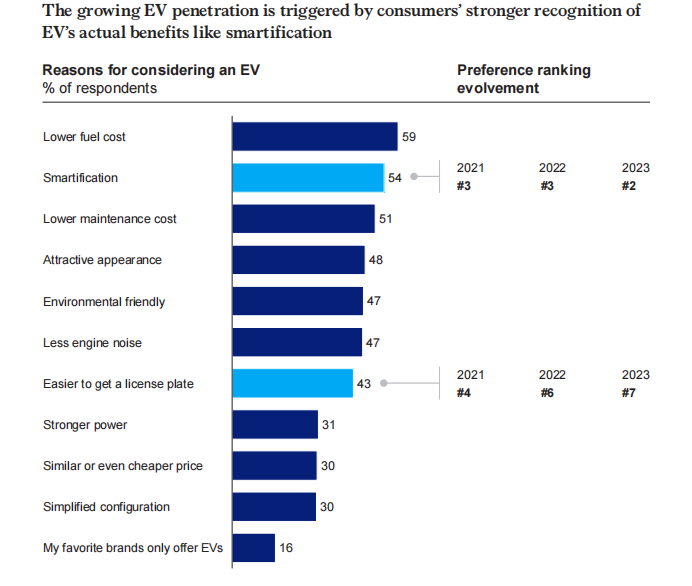

59% of the respondents chose to buy electric vehicles because they are "fuel-efficient". In addition, intelligence, low maintenance costs, and beautiful appearance are also several major factors for consumers to buy electric vehicles. In contrast, only 30% of consumers buy electric vehicles because of "stronger power". Therefore, when car company bosses talk about new products, it is always a bit thankless to highlight the zero-to-hundred acceleration performance of electric vehicles.

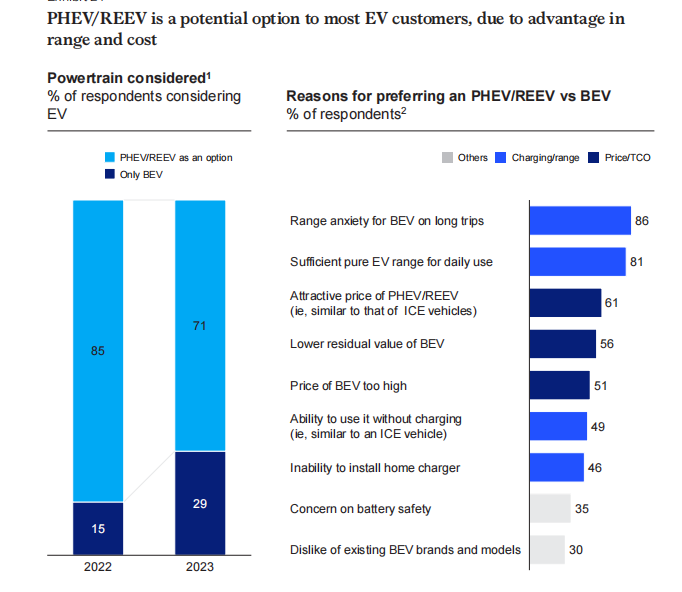

In recent years, Ideal Auto has made extended-range vehicles popular, and this low-cost power solution that can be powered by oil or electricity has become the mainstream in the market. However, the report shows that although consumers are still willing to buy extended-range and plug-in hybrid vehicles much higher than pure electric vehicles, this proportion in 2023 is lower than in 2022. The reason behind this may be the change in the license plate policy in some regions, and it may also be partly due to the improvement of the range and safety of pure electric vehicles.

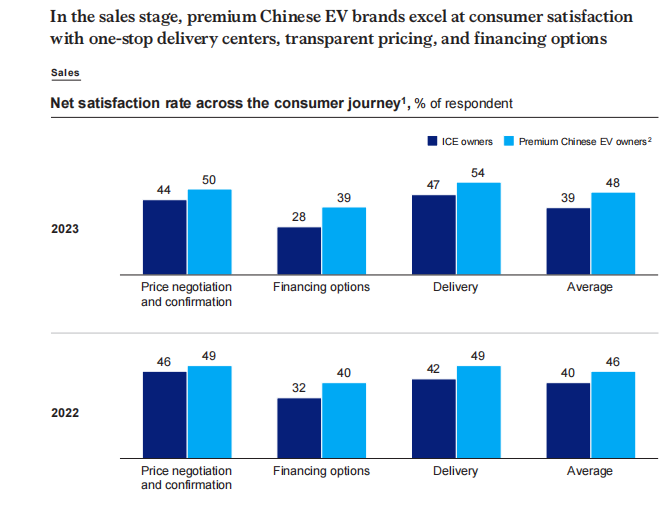

Direct sales model creates a better car buying experience

The report shows that thanks to Chinese brands, especially the direct sales model advocated by new forces, consumers' experience in the car-buying process is much better than going to traditional 4S stores. The gap is reflected in many aspects such as online information display, offline services, financial policies, delivery links, and after-sales service satisfaction.

Consumers are more accepting of assisted driving

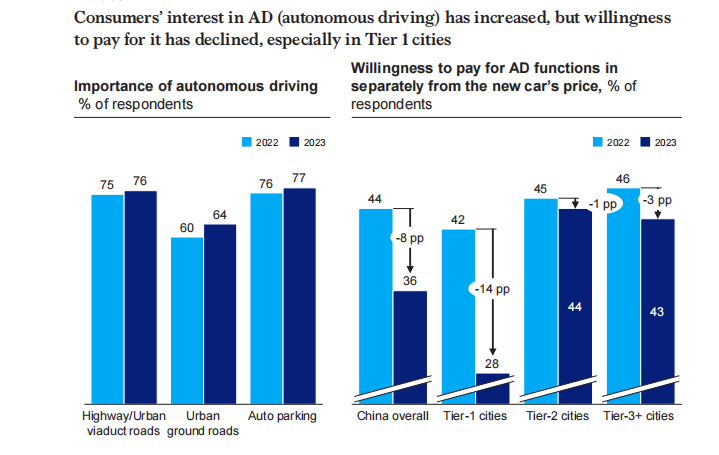

The report shows that compared with 2022, consumers' demand for use of assisted driving in highways, urban roads and parking scenarios will increase in 2023. However, users' willingness to spend money on such technologies has decreased, from 44% in 2022 to 36% in 2023. It is worth mentioning that the change in data is mainly due to the sharp decline in the willingness of users in first-tier cities to pay for it, while the willingness of users in second- and third-tier cities to pay for assisted driving remains basically unchanged.

But another related phenomenon is that among users who are willing to pay for this, users in first-tier cities prefer one-time payments, while users in second- and third-tier cities prefer more conservative "annual" or "monthly" payments.

McKinsey analysis shows that users in developed cities are more likely to be educated about new technologies earlier, and now they are able to clearly understand the functions and boundaries of assisted driving systems. Therefore, the thinking of those who are willing and unwilling to buy is very clear - either not to buy or to become a "permanent member" directly.

Relatively speaking, users in underdeveloped areas are still ignorant of assisted driving technology, and most of them buy assisted driving technology with the mentality of "giving it a try" even though they don't know how powerful it is. Therefore, there are many people willing to buy the technology, but they are unwilling to spend a large amount of money to buy the technology package at one time.

In view of the above trends, McKinsey analyzed that China's auto industry has achieved great progress through smart electric vehicles. But at the same time, the Chinese market will also make the auto industry, which has been in a low competitive intensity for a long time, "involute". It pointed out that "involute" is a painful stage that the auto industry must go through now.

Chinese consumers are the "initial culprits" of this internal circulation. Since they have evolved from passively accepting products to actively defining products, car companies need greater determination to reform to meet the current market - after all, the essence of the automotive industry is an industry that provides services to consumers.