On July 8, the Passenger Car Market Information Joint Conference (hereinafter referred to as the National Passenger Car Market Information Association) announced the car market sales in June.

Data show that in June, the national passenger car market retailed 1.767 million units, a year-on-year decrease of 6.7%, and a month-on-month increase of 3.2%; in the first half of this year, a total of 9.841 million units were sold, a year-on-year increase of 3.3%.

Among them, the retail sales of fuel vehicles in June were 910,000, a year-on-year decrease of 27% and the same as the previous month; the retail sales from January to June were 5.73 million units, a year-on-year decrease of 13%.

For comparison, the retail sales of new energy vehicles in June were 856,000, a year-on-year increase of 28.6% and a month-on-month increase of 6.4%. Retail sales from January to June were 4.111 million units, a year-on-year increase of 33.1%.

On May 9, 2024, at the International Container Terminal of Taicang Port, Jiangsu Province, new energy vehicles were waiting to be exported to overseas markets.

It is not difficult to find that the sales growth of new energy vehicles is in sharp contrast to the decline of conventional fuel vehicles. However, compared with the absolute sales volume, conventional fuel vehicles are still significantly higher than new energy vehicles. The Passenger Car Association analyzed the reason and said that new energy vehicle products are iterating quickly. In the first half of the year, there were as many as 60 new new energy vehicle products, while there were only 11 new fuel vehicle products.

The abnormal involution of the new energy vehicle market, which prefers sales to profits, has also helped the overall growth rate of new energy vehicles to surpass that of fuel vehicles.

It is worth noting that in June, there were 19 automakers with monthly wholesale sales of new energy vehicles exceeding 10,000 units, accounting for 90.4% of the total new energy passenger vehicles, compared with 88.8% last month and 82.7% in the same period last year. This means that the concentration of mainstream new energy manufacturers has further increased, and the knockout competition is in full swing.

Under the current pattern of China’s auto market, "new energy vehicle growth" is almost equivalent to "self-owned brand growth" and also means "joint-venture brand decline."

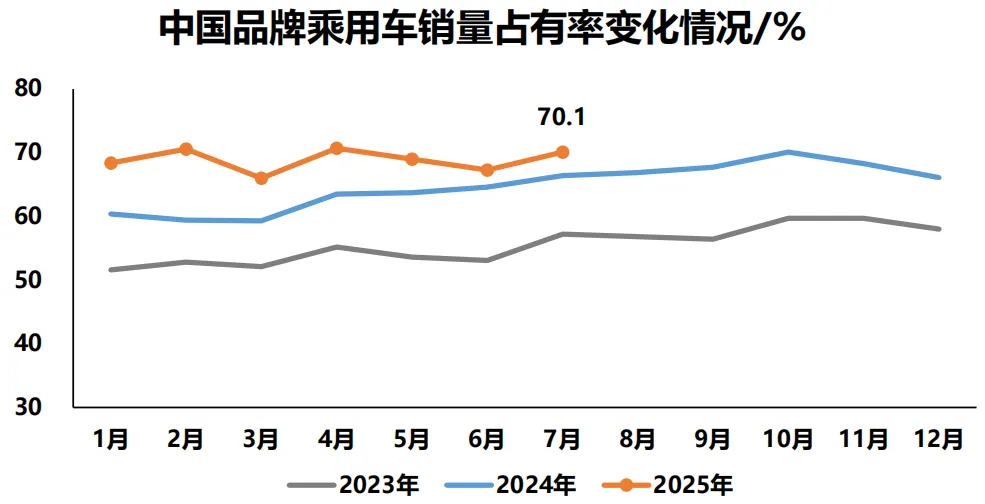

In June, self-owned brands sold 1.03 million vehicles, a year-on-year increase of 10% and a month-on-month increase of 5%. The domestic retail share of self-owned brands in that month was 58.5%, a year-on-year increase of 9.3 percentage points; the cumulative share of self-owned brands in the first half of 2024 was 57%, an increase of 7 percentage points compared to the same period last year.

In June, mainstream joint venture brands retailed 480,000 vehicles, a year-on-year decrease of 27% and a month-on-month decrease of 1%. Among them, the retail share of German brands was 18.6%, down 2.6 percentage points year-on-year; the retail share of Japanese brands was 14.3%, down 3.5 percentage points year-on-year; the retail share of American brands reached 6.3%, down 2.9 percentage points year-on-year.

Japanese brands have suffered the most serious decline.

The top 10 manufacturers in terms of retail sales in June were BYD, FAW-Volkswagen, Geely Automobile, Chery Automobile, Changan Automobile, SAIC Volkswagen, GAC Toyota, FAW Toyota, Tesla China, and BMW Brilliance. Among them, only three companies - BYD, Geely and Chery - saw sales growth, while the other seven companies all fell.

In addition, Great Wall Motors, which had frequently appeared in the top 10 lists, fell out of the top 10 in June and became the second tier of independent brands.

Under the general trend of new energy in China, the performance of emerging EV brands in June was relatively eye-catching, with Ideal and Wenjie leading the way. NIO and Leappo both exceeded 20,000 units in monthly sales.

In the export market, the situation is opposite to the domestic situation. The impact of the EU’s additional tariffs on Chinese electric vehicles has been reflected. In June, 80,000 new energy vehicles were exported, a year-on-year increase of 12.3%, but a month-on-month decrease of 15.2%. New energy vehicle exports accounted for 21% of passenger vehicle exports, down 3 percentage points from the same period last year.

On the contrary, the export volume of fuel vehicles is showing a growth trend, with a year-on-year increase of 31%.

This phenomenon gives rise to a thought - since the domestic new energy vehicle competition is so fierce and the route to the sea is not smooth, but fuel vehicles have great potential overseas, should automakers reconsider the proportion of resource investment in fuel vehicles and electric vehicles? Already?