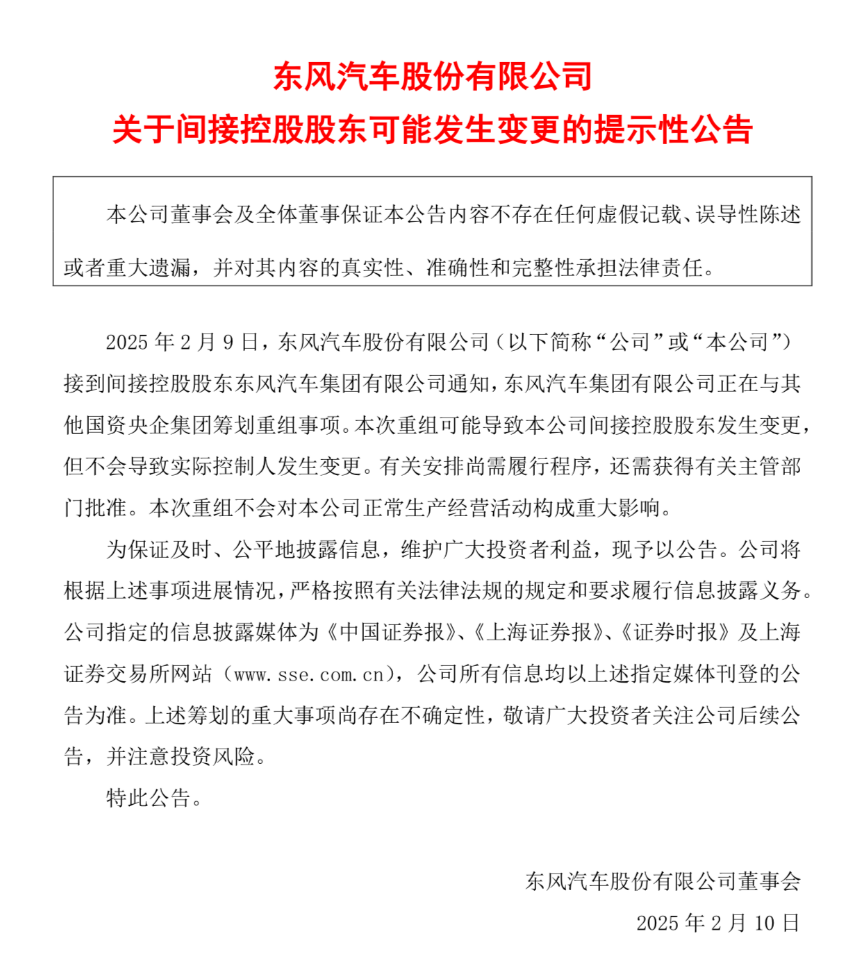

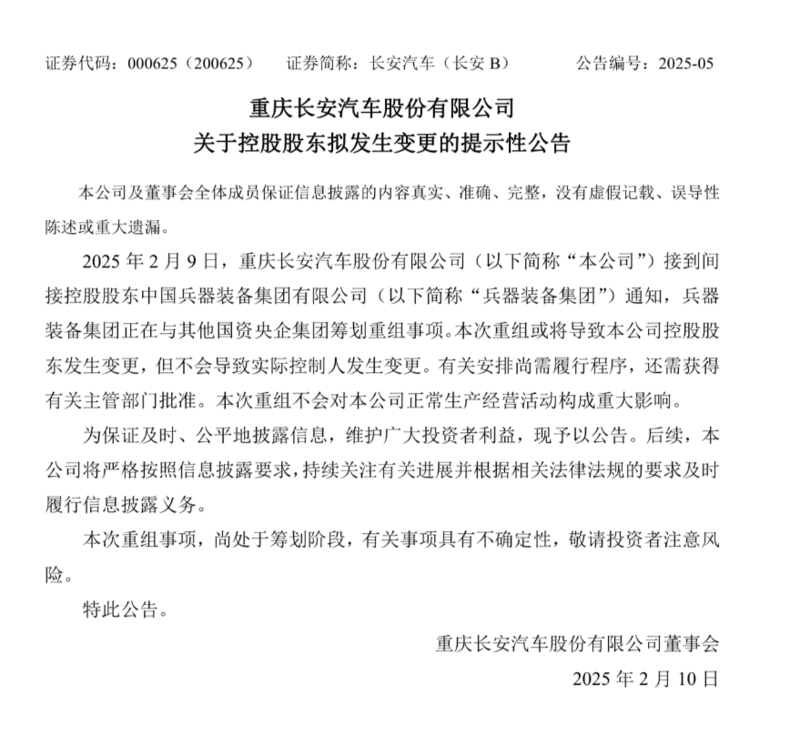

On February 9, 2025, several listed companies under Dongfeng and Changan issued an announcement, disclosing that the indirect controlling shareholders (Dongfeng Group and China North Industries Group Corporation) are planning a restructuring involving the company.

Although the announcement did not specify the details of the merger, it emphasized that the actual controller after the reorganization will still be the State-owned Assets Supervision and Administration Commission, and that "normal production and operations will not be affected."

The background of this action is closely related to the SASAC's policy orientation in recent years to promote the professional integration of central enterprises. In 2024, the SASAC explicitly required separate assessments of the new energy vehicle businesses of the three central enterprises, FAW, Dongfeng and Changan, with the aim of breaking through core technology bottlenecks through concentrated resources and changing the current situation of state-owned auto companies being "big but not strong."

At present, the Chinese auto market has shifted from the "joint venture bonus period" to the "self-owned brand elimination competition". In 2024, the market share of self-owned brands will exceed 60%, but the pace of new energy transformation of state-owned auto companies lags behind private companies such as BYD and Geely. If Dongfeng and Changan merge, the space for resource integration between the two parties in terms of technology, supply chain, market channels and other dimensions will become a key driving force.

In terms of technical collaboration, Dongfeng has deployed the smart luxury Lantu and hardcore off-road Mengshi brands in the field of high-end electrification, while Changan covers the mid- and high-end markets through the cost-effective Deep Blue brand and Avita, which is supported by Huawei and CATL. The two sides are significantly complementary in the fields of three-electric systems and intelligent driving: for example, Dongfeng's solid-state battery research and development can make up for Changan's previous battery technology shortcomings. Of course, with the release of Changan's Golden Bell Battery, the two sides can be said to complement each other in this field, rather than one side feeding; and Changan's high-end intelligent driving system based on Huawei ADS, if opened to Dongfeng, can accelerate the latter's intelligent transformation. In addition, if the patent reserves of both parties in hybrid technology are shared, the research and development costs can be greatly reduced.

The supply chain is a cost "black hole" for enterprises. Otherwise, He Xiaopeng would not have been told by Wang Fengying that "steel was too expensive" and "it took nine months to figure it out". In this regard, Dongfeng and Changan have overlapped in the procurement of core components such as batteries and chips, and they both cooperate with CATL. The large-scale bargaining power after the merger may change the discourse power of the supply chain.

In terms of production bases, if Dongfeng's production capacity in Hubei and Guangdong and Changan's layout in Chongqing and Hefei can be coordinated and allocated, it will not only alleviate the pressure of regional overcapacity, but also concentrate production at coastal bases to meet export demand and reduce logistics costs.

Let's look at the channels. Dongfeng has outstanding advantages in the traditional 4S network and commercial vehicle channels in first- and second-tier cities, while Changan has accumulated experience in new energy user operations through the direct sales model of the Deep Blue brand. After the merger, Dongfeng can reach young people through Changan's digital direct sales system, and Changan can use Dongfeng's commercial vehicle channels to develop the B-end market. In terms of overseas layout, Dongfeng has a foundation in Europe through cooperation with Stellantis, while Changan focuses on the Southeast Asian market. After the merger, the two parties can form a two-line overseas strategy of "high-end market + emerging market" to disperse geopolitical risks.

The reconstruction of brand positioning is another key to avoid internal friction. Currently, the two sides have overlapping products in the price range of 150,000 to 300,000 yuan, which reflects the strategic anxiety of state-owned auto companies in the process of transformation: "both maintaining the basic market and seizing new tracks."

In the hybrid market, Dongfeng Fengshen Haohan (priced at RMB 89,900-136,900) and Changan UNI-V iDD (RMB 144,900-159,900) are in direct competition with each other at around RMB 150,000. Both of them focus on "long-range plug-in hybrid + sporty design", and their target customer groups are highly overlapping, both targeting young families' first-time buyers.

In the field of pure electric SUVs, although the price ranges of Dongfeng Lantu FREE (starting from RMB 266,900) and Changan Avita 11 (RMB 300,000-400,000) are misaligned, Lantu Light Chasing EV (starting from RMB 252,800) and Avita 12 (starting from RMB 300,800) are in close competition in the RMB 250,000-300,000 range. Both emphasize "luxury and intelligence", but Lantu relies on traditional luxury genes, while Avita focuses on Huawei's Hongmeng ecosystem. The differentiation has not yet been fully perceived by consumers.

In terms of fuel vehicles, Dongfeng Fengshen Yixuan MAX (97,900-137,900 yuan) and Changan Ruicheng PLUS (99,900-122,900 yuan) are competing for existing users in the 100,000 yuan fuel vehicle market, but this market is being squeezed by plug-in hybrid models such as BYD Qin PLUS DM-i.

The essence of the integration behind the overlapping price bands is an upgrade from "involution to outward expansion". In the short term, it is necessary to bear the pain of shrinking product lines, but in the long term, it is possible to create hot products by concentrating resources. Referring to the experience of Geely's merger with Volvo, SAIC's merger with Nanjing Automobile, and GAC's merger with Nanfeng, if both parties can retain the independent brand tone but deeply cooperate in platform architecture, supply chain, and user operations, the overlapping price bands can become a "moat" covering multiple needs.

Although the integration logic is clear, it is not easy to implement in practice. As far as the integration of management structures is concerned, Dongfeng is a long-established central enterprise with a complex decision-making hierarchy, and Changan has been more radical in its market-oriented reforms in recent years. The conflict in management styles between the two parties may affect efficiency.

If this restructuring is implemented, it will send two major signals. First, state-owned auto companies will shift from "scale expansion" to "core capability aggregation" and impact the discourse power of the new energy industry chain through resource concentration. Second, the trend of "the strong will always be strong" in the auto industry will intensify, and small and medium-sized auto companies lacking technology or funds may be eliminated faster.

However, the industry generally believes that the probability of a direct merger between Dongfeng and Changan is low, and the more likely path is to achieve a change in controlling shareholders through capital operations led by the State-owned Assets Supervision and Administration Commission, thereby promoting the gradual integration of key links such as technology and supply chain. This "strategic coordination + independent operation" model can not only avoid the shock of large-scale mergers, but also gradually release synergy effects.

As for the rumors reported by some self-media such as "a new group will be established in the future, and there will no longer be two major automobile groups, Dongfeng and Changan" and "the leadership team of the new automobile group has been determined", no response has been received from either party.